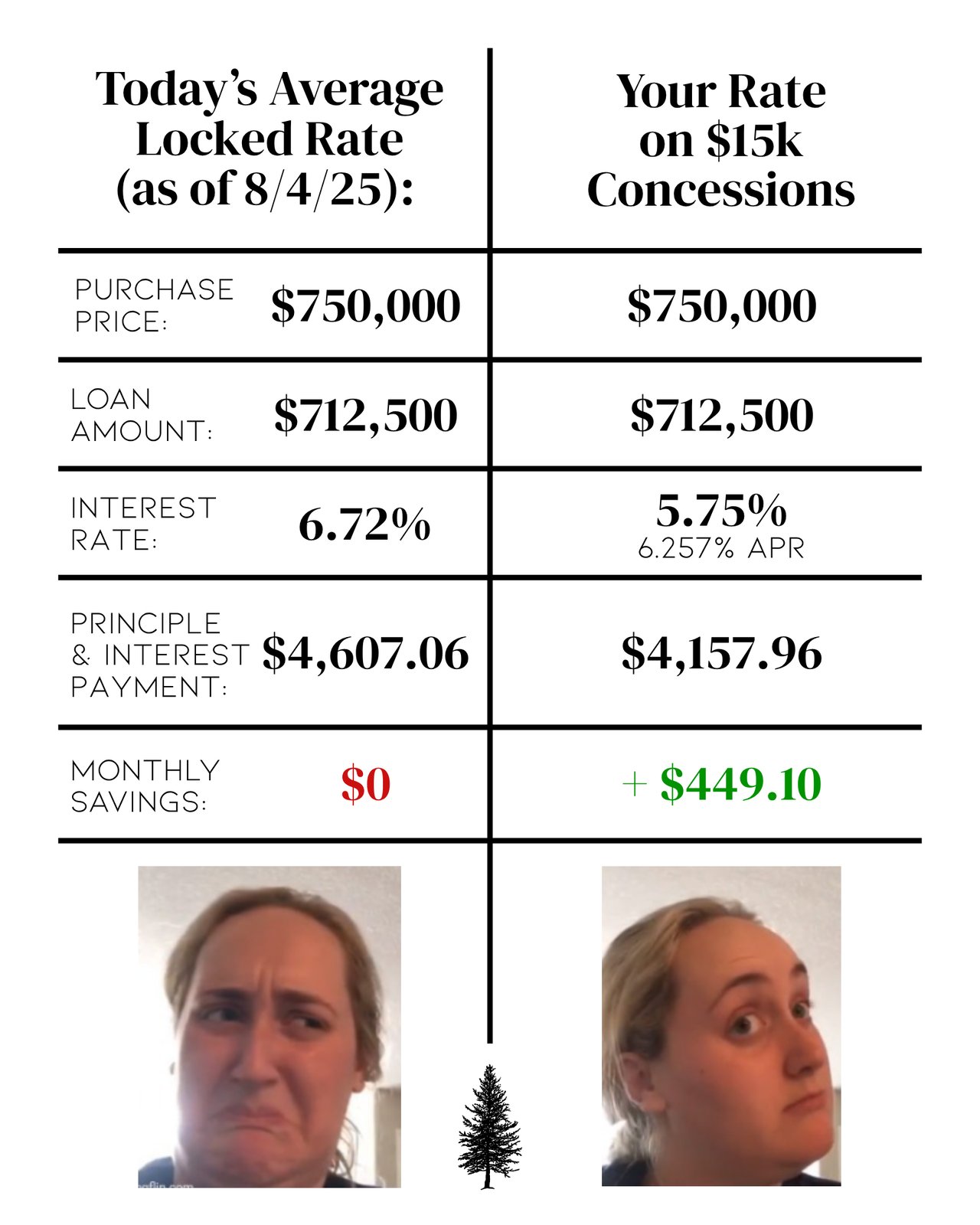

We’re seeing a continued window of opportunity for buyers to purchase in a softer market while leveraging seller concessions—which are essentially cash credits from the seller that buyers can use to cover closing costs, permanently buy down their rate, or opt for a temporary buy down (like the 2-1 program, where your starting rate is 2% lower in year one and 1% lower in year two). Over half of transactions today include some form of seller-paid credit—but that trend may not last deep into 2025.

Looking ahead, there’s increasing political pressure—particularly from the Republican side—to remove current Fed Chair Jerome Powell from office. Their agenda also includes slashing the federal funds rate by 2–3% in short order. While mortgage rates aren’t directly tied to the federal funds rate, they’re close cousins—and historically tend to move in the same direction. If Powell is ousted, we could see a sharp dip in rates by mid to late next year.

So, what does that mean for today’s buyers? The real investment is made on the buy. You can never change the price you paid for a home—but you can always change your rate. Buying now with seller concessions gives you the ability to hedge against today’s rates while keeping the door open to refinance if rates drop. And when that happens, the market is likely to shift again—bidding wars return, equity climbs, and seller generosity fades.

The smartest move? Take advantage of sellers who are stuck in this slower Q4 market and willing to offer concessions. It’s a short-term win and a long-term play.

Austin Beger

Mortgage Loan Officer

NMLS 2004656

Adam Hothersall

Business Development

NMLS 2521091